Money is about to enter a new era of competition

Digital technology is poised to change our relationship with money and, for some countries, the ability to manage their economies.

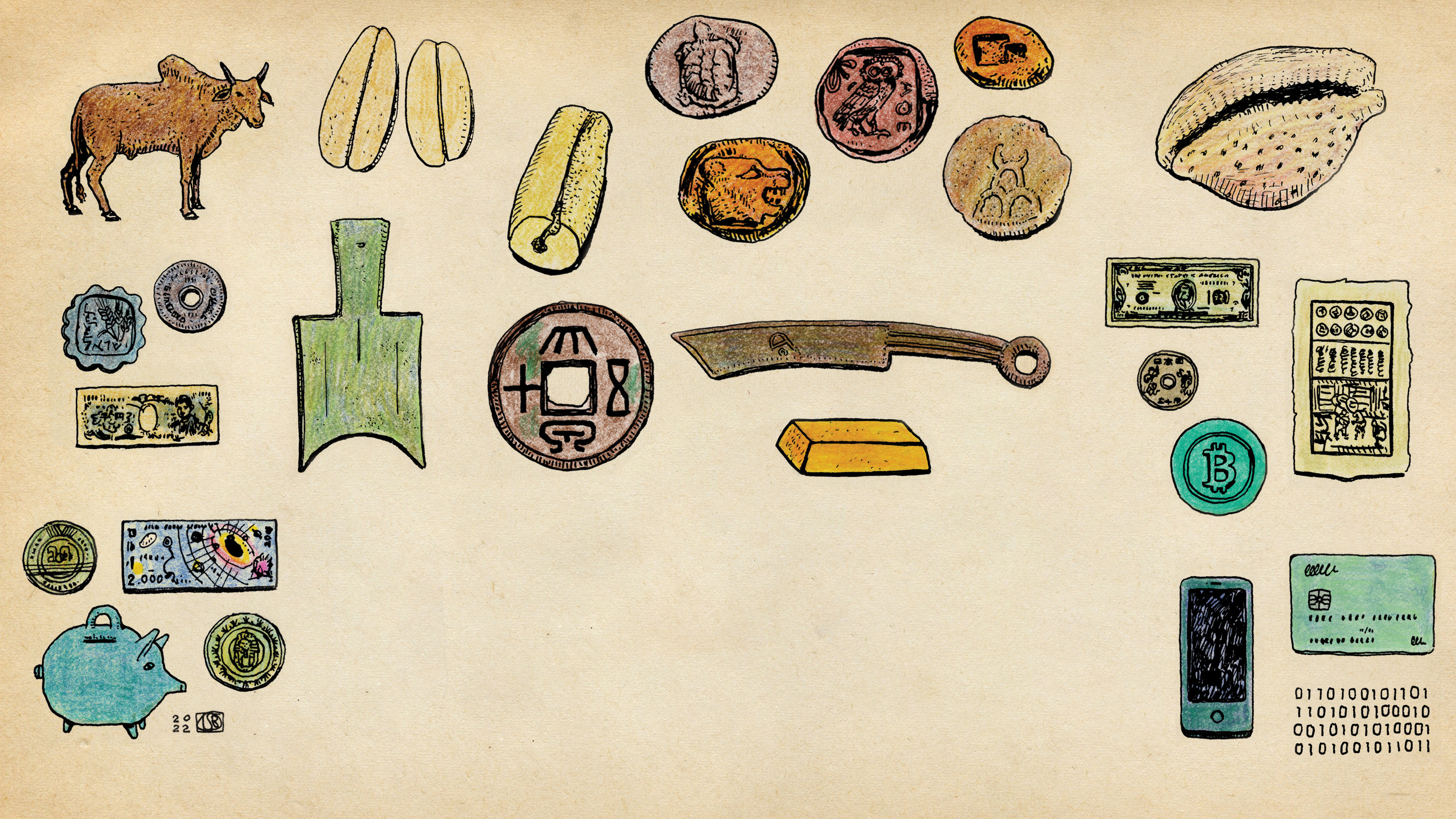

Money is one of humankind’s most remarkable innovations. It makes it possible to trade products and services across great geographic distances, between people who may not know each other and have no particular reason to trust each other. It can even be used to transfer wealth and resources over time. Without money, trade and commerce—all human economic activity, really—would be severely constrained in terms of time and space.

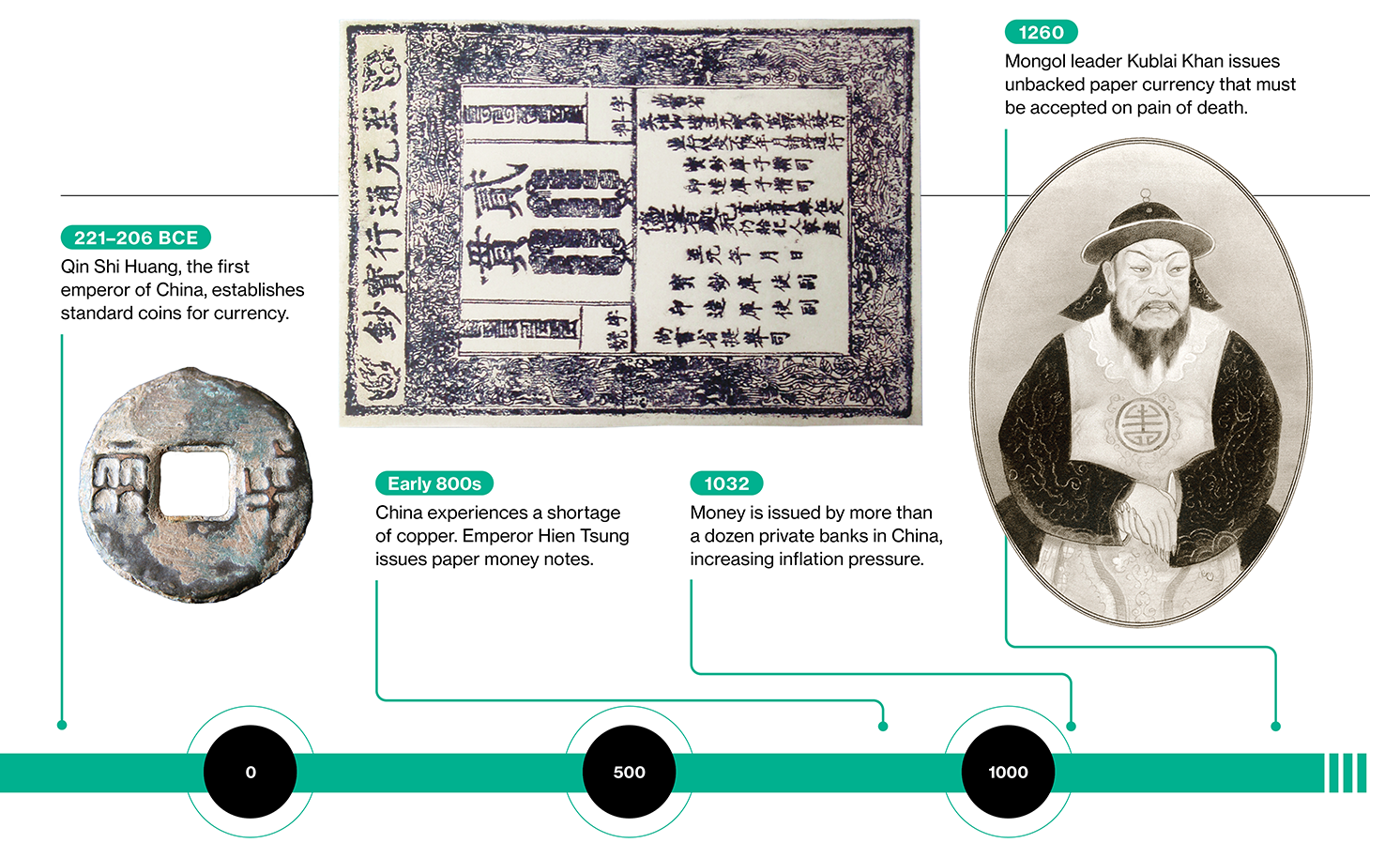

The privilege of issuing money is synonymous with economic power. So it should come as little surprise that history is replete with examples of currency competition, both within countries and between them. In China, home of the world’s first paper money, currencies issued by private merchants and provincial governments competed for many centuries. Indeed, banknotes issued by governmental and private banks coexisted in China as late as the first half of the 20th century.

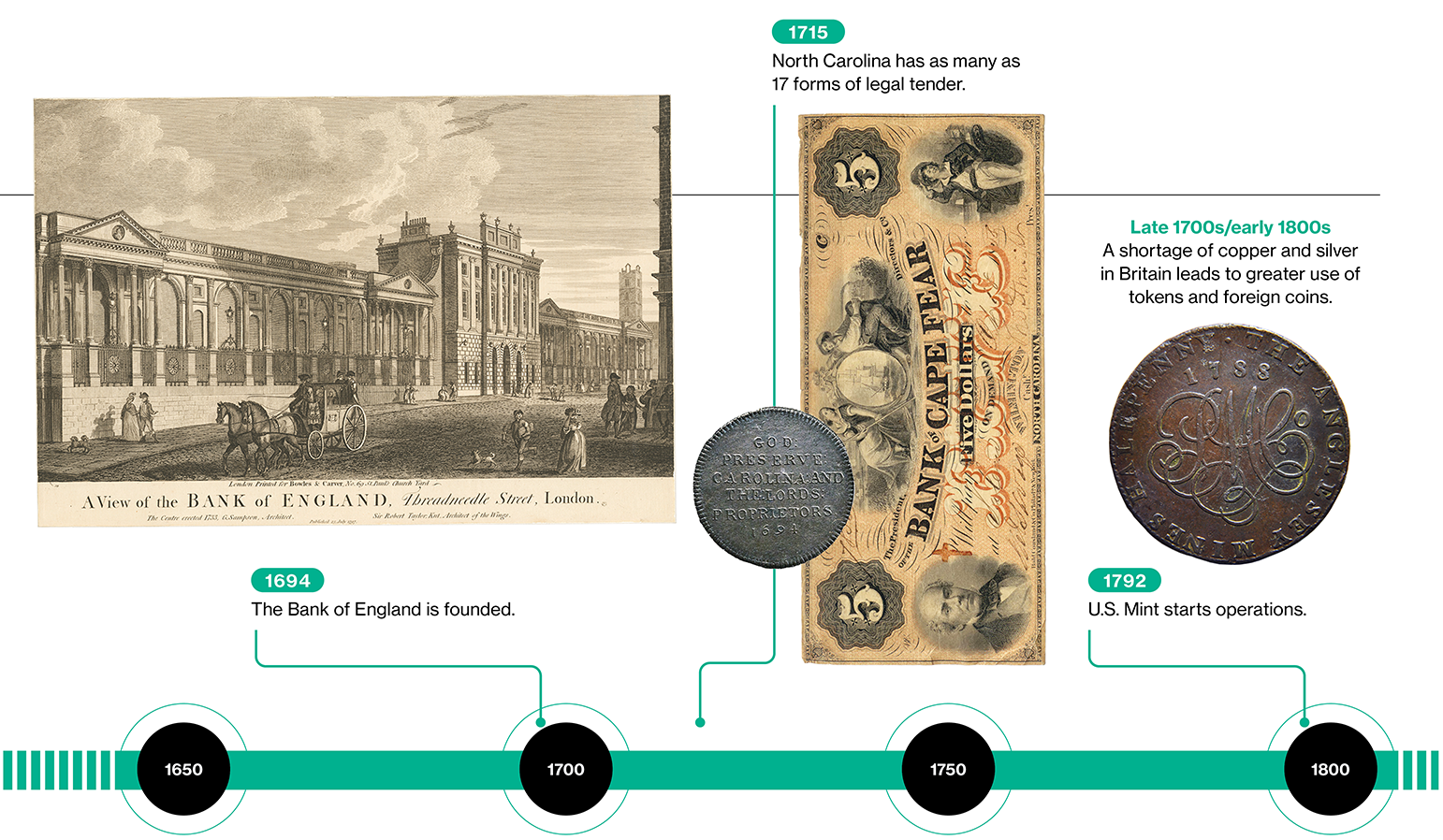

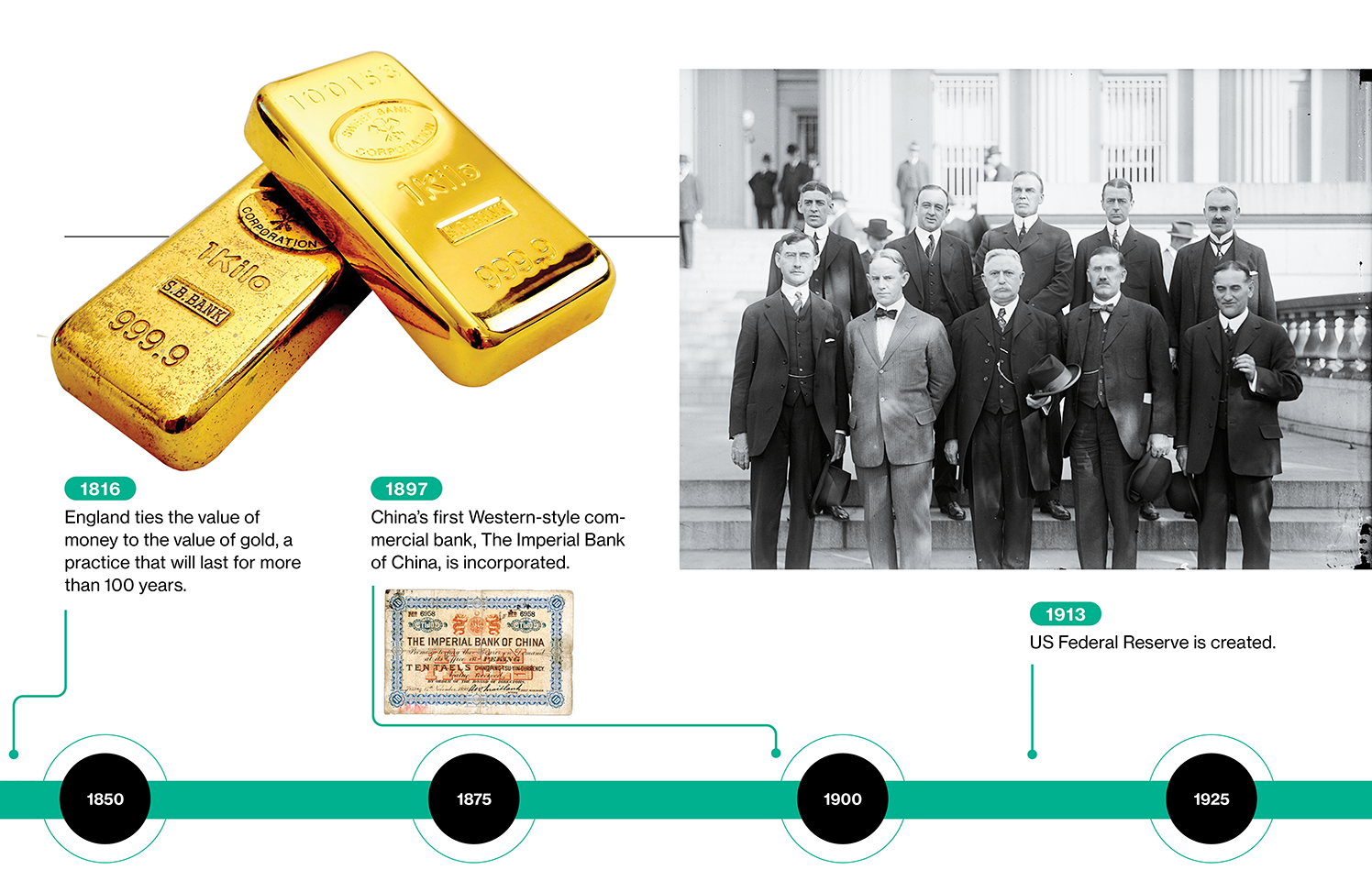

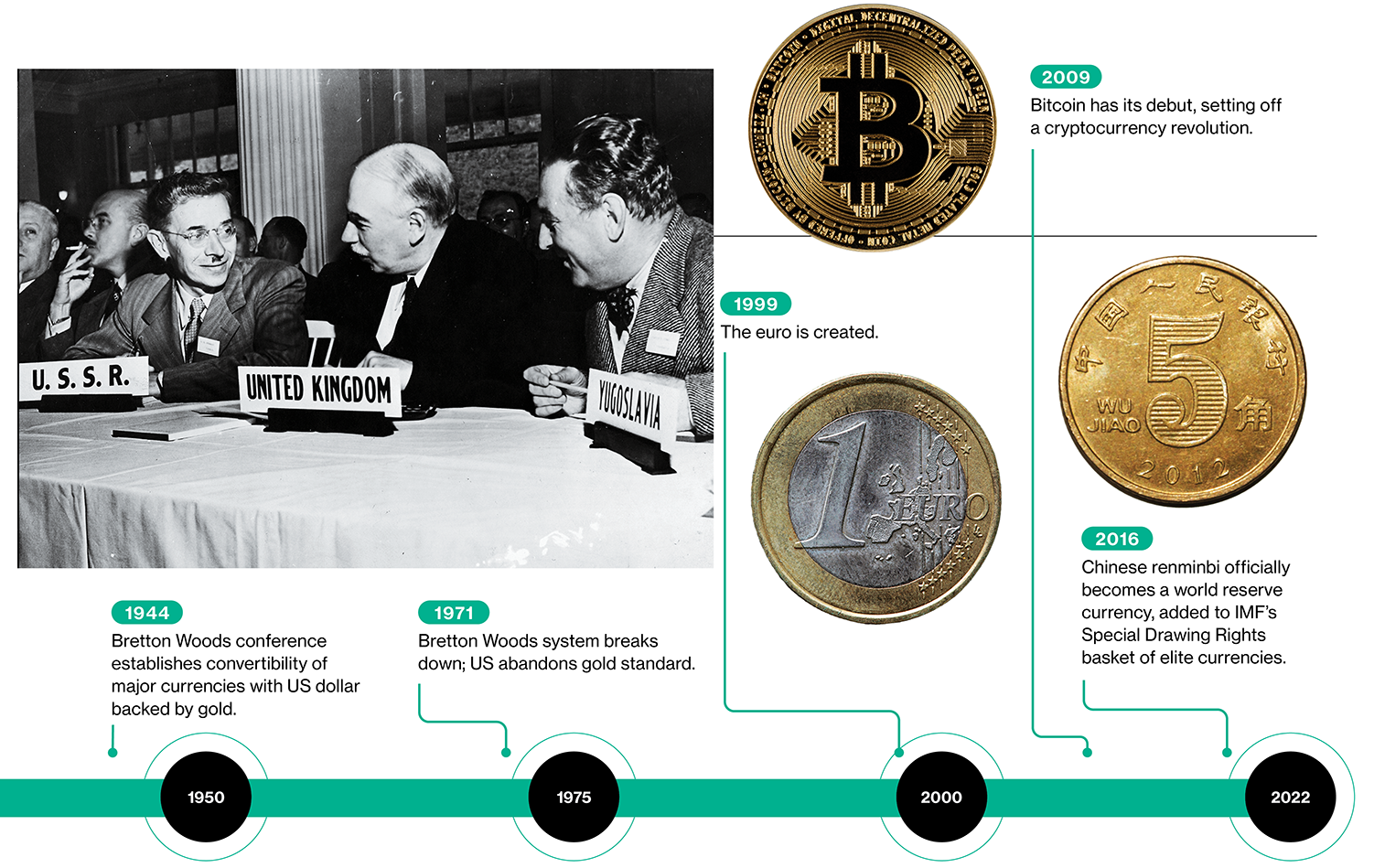

What finally, decisively ended this competition was the emergence of central banks, which were given the exclusive privilege of issuing legal currency and tasked with maintaining its stability. This shift happened quite early in Sweden; the world’s oldest central bank, the Riksbank, was established there in the 17th century. In China, competition closed with the founding of the People’s Bank of China in 1948, shortly before the formal creation of the People’s Republic of China. Since the central banks stepped in, competition has been mostly international, with the relative value of currencies depending on the reputation and stability of the central banks issuing them.

We now stand at the threshold of another era of upheaval. Cash is on the way out, and the digital technologies that are replacing it could transform the very nature and capabilities of money. Today, central-bank money serves at once as a unit of account, a medium of exchange, and a store of value. But digital technologies could lead those functions to separate as certain forms of private digital money, including some cryptocurrencies, gain traction. That shift could weaken the dominance of central-bank money and set off another wave of currency competition, one that could have lasting consequences for many countries—particularly those with smaller economies.

In ancient societies, objects such asshells, beads, and stones served as money. The first paper currency appeared in China in the seventh century, in the form of certificates of deposit issued by reputable merchants, who backed the notes’ value with stores of commodities or precious metals. In the 13th century, Kublai Khan introduced the world’s first unbacked paper currency. His kingdom’s bills had value simply because Kublai decreed that everyone in his domain had to accept them for payment on pain of death.

Kublai’s successors were less disciplined than he was in controlling the release of paper currency. Subsequent governments in China and elsewhere gave in to the temptation of printing money recklessly to finance government expenditures. Such wantonness typically leads to surges of inflation or even hyperinflation, which in effect amounts to a precipitous fall in the quantity of goods and services that a given sum of money can buy. This principle is relevant even in modern times. Today, it is trust in a central bank that ensures the widespread acceptance of its notes, but this trust must be maintained through disciplined government policies.

To many, however, cash now seems largely anachronistic. Literally handling physical money has become less and less common as our smartphones allow us to make payments easily. The way in which people in wealthy countries like the United States and Sweden, as well as inhabitants of poorer countries like India and Kenya, pay for even basic purchases has changed in just a few years. This shift may look like a potential driver of inequality: if cash disappears, one imagines, that could disenfranchise the elderly, the poor, and others at a technological disadvantage. In practice, though, cell phones are nearly at saturation in many countries. And digital money, if implemented correctly, could be a big force of financial inclusion for households with little access to formal banking systems.

Cash still has some life in it. During the covid pandemic, even as contactless payments became more prevalent, the demand for cash surged in major economies including the US, presumably because people viewed it as a safe form of savings. Many states in the US have laws in place to make sure that cash is accepted as a form of payment, something that would protect people who cannot or do not want to pay through other means. But consumers, businesses, and governments have generally welcomed the shift to digital forms of payment, especially as new technologies have made them cheaper and more convenient.

The decline of physical cash, once valued as the most definitive form of money, is but a small feature of the rapidly changing financial landscape, though. One of the most dramatic forces of change has been the rise of cryptocurrencies, which have shaken long-held precepts about money and finance.

Bitcoin, the cryptocurrency that started it all, may not have much of a role to play in this monetary future.

Bitcoin was designed to enable people to complete transactions pseudonymously (using only digital identities rather than real ones) and without the intervention of a trusted third party such as a central bank or financial institution. In other words, anyone with a computer could conduct transactions—no credit card or bank account necessary. Coins are issued and transactions validated through a computer algorithm that runs autonomously; the identity of its creator remains unknown to this day.

The timing of Bitcoin’s introduction in early 2009, when the global financial crisis had decimated trust in governments and banks, could not have been better. But even as it gained in popularity, Bitcoin stumbled in its basic uses. The volatility of Bitcoin’s value, with wild price swings from one day to the next, has made it an unreliable method of payment. Moreover, it turns out that the cryptocurrency does not guarantee anonymity—users’ digital identities can, with some effort, be connected to their real identities (in some ways this is a good thing, as Bitcoin transactions that once fueled the dark web, where unsavory and illicit commerce is conducted, have fallen sharply). Today, Bitcoin and other cryptocurrencies like it have mostly become speculative financial assets, with little intrinsic worth and sky-high valuations that are not backed by anything other than investors’ faith.

A new generation of cryptocurrencies is emerging that promises to fix many of Bitcoin’s flaws. Stablecoins, cryptocurrencies whose stable value comes from being backed by reserves of US dollars or other reputable fiat currencies, are proliferating. Stablecoins are billed as reliable, easily accessible digital payment systems that will make both domestic and international payments cheaper and quicker. However, unlike Bitcoin, which is fully decentralized, they require transactions to be validated by the issuing institution—which could be a bank, a corporation, or just an online entity. This means users must trust that institution to validate only legitimate transactions and hold adequate reserves, and regulators currently do not require independent verification of either of those actions. Thus, despite their laudable goal of meeting the demand for better payment systems, stablecoins have raised a raft of concerns.

Even with all these growing pains, the cryptocurrency revolution has expanded the frontiers of digital payment technologies and helped light a fire under central banks. Long viewed as conservative institutions resistant to major change, many are now entering the digital race.

Faced with the increasing irrelevance of their paper currencies, many central banks around the world are looking to issue their money in digital form. Major economies such as China, Japan, and Sweden are experimenting with central-bank digital currencies (CBDCs), which in effect are just digital versions of the currencies they now issue as notes and coins. The Bahamas and Nigeria have already rolled out their CBDCs nationwide. Countries including Brazil, India, and Russia are in the process of initiating their own experiments.

Some countries see CBDCs as a way to broaden access to the formal financial system—even households without bank accounts or credit cards would gain access to a safe and inexpensive digital payment system. Other countries are pursuing CBDCs to increase the efficiency and stability of digital payment systems. Sweden’s e-krona is being pitched as a backstop in case the payment system managed by private-sector companies, which might work perfectly well under most circumstances, should fail because of either technical problems or confidence issues.

CBDCs could also help maintain the relevance of central-bank retail money in countries where digital payments are becoming the norm. China, for example, is pursuing its digital renminbi at a time when two financial titans, Alipay and WeChat Pay, are striving to dominate the payment landscape.

CBDCs have many other advantages, too. They could bring certain types of economic activity out of the shadows and into the tax net (unlike cash transactions, which often go unreported to tax authorities), reduce counterfeiting, and make it harder to use official money for illicit purposes such as money laundering, drug trafficking, and financing of terrorism. But they could threaten whatever minimal vestiges of privacy we still enjoy—after all, everything digital leaves a trace. Transactions using CBDCs are likely to be auditable and traceable, as no central bank would want to allow its money to be used for illicit transactions.

What will the world of money look like in five or 10 years’ time? We could envision a world where many people hold digital wallets with a mix of money in traditional bank accounts, stablecoins managed by private companies, and perhaps one or more CBDCs, moving them around depending on global conditions. Then again, no one knows how well stablecoins and CBDCs will coexist. Meta (formerly Facebook), for example, had planned to roll out its own stablecoin. But the project was quashed by US regulators, who were concerned about Meta’s objectives and about the possibility that the stablecoin could be used to finance illicit transactions within and across national borders.

The basic case for stablecoins as more efficient and easily accessible forms of digital payment could be undercut by CBDCs. For the moment, stablecoins seem to be holding their own—there were more than 30 in circulation as of March 2022, with a total value of about $185 billion. And there is the possibility that stablecoins built on top of large-scale commercial ecosystems such as Amazon’s could gain significant traction as means of payment.At any rate, insofar as their stability depends on their being backed by fiat currencies, stablecoins are unlikely to become independent stores of value. In other words, they would be used primarily because they would be cheaper or more convenient means of payment.

However it plays out, the digital-currency revolution is going to have implications for the international monetary system. Take cross-border payments, which are inherently complicated because they involve multiple currencies, institutions using different technological protocols, and varying sets of regulations. All this makes international payments slow, expensive, and difficult to track in real time. Cryptocurrencies, which can be shared freely across borders, will reduce these impediments, enabling nearly instantaneous payment and settlement. Even CBDCs could ease the frictions if they are made available for use internationally and gain widespread acceptance.

More-efficient international payment systems will bring a host of benefits. For one thing, they will make it easier and cheaper for economic migrants to send remittances back to their home countries—a process that currently costs an average of 6% of the transaction amount, according to the World Bank. The estimated costs are even higher for remittances going to low-income countries, many of which depend on such inflows for a large share of national income.

In principle, financial capital will be able to flow more easily within and across countries to the most productive investment opportunities, raising global economic welfare—at least as measured by GDP and consumption capacity. But easier capital flows across national borders will also pose risks for many countries, making it much harder to manage their exchange rates and their economies.

The resulting challenges will be especially thorny for smaller and less developed countries.

National currencies issued by their central banks, particularly those currencies seen as less convenient to use or more volatile in value, could be displaced by private stablecoins and perhaps also by CBDCs issued by the major economies. This would result in a loss of monetary sovereignty: less prominent central banks would lose control over the circulation of money in their economies. The phenomenon of “dollarization,” wherein a trusted foreign currency supplants a volatile domestic currency (long the bane of many Latin American countries), could be intensified by the proliferation of digital currencies. In places such as Iran and Turkey, we have already seen people use cryptocurrencies to get around restrictions on capital outflows when currencies were plunging in value, enabling them to spirit funds out of their countries and into safer investments abroad.

Even for the major reserve currencies, there are some shifts in store, though the long-standing dream of many governments around the world—knocking the US dollar off its pedestal as the dominant global reserve currency—will probably remain just that for the foreseeable future. Indeed, it is likely that stablecoins backed by the dollar will gain widespread acceptance relative to stablecoins backed by other currencies, indirectly increasing its relative prominence. But the digital renminbi is poised to gain traction as a method of payment, and even a gradual and modest increase in the renminbi’s use, along with a rise in stablecoins, could reduce the importance of other reserve currencies, including the euro, the British pound sterling, the Japanese yen, and the Swiss franc.

When it comes to money’s function as a medium of exchange, we can expect more competition between private and fiat currencies. In principle, this should lead to payments that are cheaper and quicker—benefiting consumers and businesses—while also motivating issuers, whether private or official, to exercise discipline in order to preserve the value of their currencies.

But it is worth keeping in mind that technology can have unpredictable consequences. Rather than leading to a proliferation of private and official currencies that compete on a level playing field, the digitization of currencies could make economic power even more concentrated. If major currencies such as the dollar, the euro, and the renminbi are easily available worldwide in digital form, they might displace the currencies of smaller and less powerful nations. Digital currencies issued by large corporations, taking advantage of the companies’ already dominant commercial or social media ecosystems, might gain traction too. Unless they are quashed by governments, they could one day turn into independent stores of value by giving up their fiat-currency backing. This could create even more monetary instability if individual countries wound up having multiple issuers of money, with competing domestic currencies fluctuating in value relative to one another.

All that is certain is that the international monetary system is on the threshold of momentous change wrought by the digital revolution. It remains to be seen whether this ultimately benefits humanity at large—or exacerbates existing domestic and global inequities.

Eswar Prasad is a professor in the Dyson School at Cornell University, a senior fellow at the Brookings Institution, and author of The Future of Money: How the Digital Revolution Is Transforming Currencies and Finance.

Deep Dive

Humans and technology

Building a more reliable supply chain

Rapidly advancing technologies are building the modern supply chain, making transparent, collaborative, and data-driven systems a reality.

Building a data-driven health-care ecosystem

Harnessing data to improve the equity, affordability, and quality of the health care system.

Let’s not make the same mistakes with AI that we made with social media

Social media’s unregulated evolution over the past decade holds a lot of lessons that apply directly to AI companies and technologies.

Stay connected

Get the latest updates from

MIT Technology Review

Discover special offers, top stories, upcoming events, and more.