Ethereum thinks it can change the world. It’s running out of time to prove it.

It’s late October. Outside the sprawling Prague Congress Centre, not only is the weather turning, but the cryptocurrency world is crashing down, as it has been for much of this year. Expectations for blockchain systems, sky-high just a year ago, are falling nearly as fast as prices for the coins based on them. But inside, the mood is rather different. Here, Devcon—the annual “family reunion” organized by the Ethereum Foundation—is in full swing, and there’s barely a hint of negativity to be found.

On the contrary, there is lots of hugging, unicorn-themed clothing, and a sense of excitement about the future. This crowd doesn’t give a damn about what’s happening outside. Whatever’s going on in here, it’s about much more than magic internet money.

Ethereum is already the most famous cryptocurrency after Bitcoin and the third largest in total value. Unlike the others, however, it aims to serve as a general-purpose computing platform that could, its adherents believe, make possible entirely new forms of social organization. The central topic of Devcon is “Ethereum 2.0,” a radical upgrade that would finally allow the network to realize its true power.

The nagging truth, though, is that all the positivity in Prague masks daunting questions about Ethereum’s future. The handful of idealistic researchers, developers, and administrators in charge of maintaining its software are under increasing pressure to overcome technical limitations that stymie the network’s growth. At the same time, well-funded competitors have emerged, claiming that their blockchains perform better. Crackdowns by regulators, and a growing understanding of how far most blockchain applications are from being ready for prime time, have scared many cryptocurrency investors away: Ethereum’s market value in dollars has fallen more than 90% since its peak last January.

The reason Devcon feels so upbeat despite these storm clouds is that the people building Ethereum have something bigger in mind—something world-changing, in fact. Yet to achieve its goal, this ragtag community needs to crack a problem as complicated as any of the toe-curling technical challenges it faces: how to govern itself. It must find a way to organize a scattered global network of contributors and stakeholders without sacrificing “decentralization”—the principle, which any cryptocurrency community strives for, that no one entity or group should be in control.

Is this even possible? Other blockchain communities, including Bitcoin, have struggled with infighting and gridlock over the kinds of major software upgrades Ethereum is planning. Whether the community can make Ethereum 2.0 happen isn’t just important for crypto speculators and blockchain nerds: it may just go to the very heart of how society is run.

The CryptoKitties effect

To understand the hype around Ethereum, you first need to understand the hype around blockchains in general, and then what makes Ethereum different. (Skip the next four paragraphs if you already know.)

A blockchain is essentially a shared database, stored in multiple copies on computers around the world. These computers are known as “nodes,” and any computer on the internet can become a node in a blockchain network by installing and running specially developed software. What makes a blockchain different from a regular database is that, thanks to the innovative use of cryptography, there is no need for a central authority like a bank or government to maintain it. The nodes run the software, and collectively they make sure every new transaction follows certain rules before adding it to the blockchain.

This process, called mining, requires a lot of computing. That makes it very hard to tamper with the blockchain’s record of transactions, since doing so generally depends on controlling most of the network’s mining power, and that would require an enormous expenditure of resources. Hence the ideal blockchain is “decentralized,” i.e., it has lots of independent users so nobody is in control.

The first blockchain application was Bitcoin, a system for peer-to-peer payments. Ethereum goes an ambitious step further. Instead of just processing and storing currency transactions, its nodes are supposed to collectively function as a “world computer” on which, using specialized programming languages, people can build applications that are supposed to look and feel much like the ones already on our phones—except no one is in charge of them.

These decentralized applications, or “dapps,” might include such things as voting systems, trading markets, or even social networks—imagine a Twitter or Facebook that nobody owns. Being decentralized, they would theoretically be immune to attempts to manipulate them or shut them down. For Ethereum’s most avid believers, these contain the promise of an entirely new kind of democratic society in which it is much harder to concentrate wealth and power, hide corruption, and exert shady, behind-the-scenes influence.

A year ago—practically centuries in crypto time—investors were pouring billions of dollars into promising projects building dapps. They invested via initial coin offerings, in which blockchain company founders raise money, crowdfunding-style, by selling digital tokens. Prices for coins, including Ether, Ethereum’s own crypto-token, were soaring. Many of their fans believed blockchains and cryptocurrencies were going to swiftly displace traditional financial intermediaries, upend monopolistic internet companies, and decentralize the web.

Then came CryptoKitties.

Perhaps it’s appropriate that a childish game was the thing to kill the mood. CryptoKitties, launched in late 2017, are colorful cartoon cats—like digital versions of Beanie Babies, the plush toy animals that became a collecting craze in the 1990s. Like Beanie Babies, CryptoKitties are all unique in some way, but unlike Beanie Babies, they can reproduce. Each kitty’s uniqueness is verified on the Ethereum blockchain using a special kind of token, and players can buy, sell, or “breed” cats using Ether.

The problem was that CryptoKitties got too popular too fast. As with Beanie Babies, some kitties became highly prized, trading hands for as much as $170,000 worth of Ether. The mad rush to breed them led to a sudden sixfold increase in transaction volume that clogged the network and slowed Ethereum to a halt. It exposed the truth: the technology is immature, incapable of handling the kinds of workloads that big dapps would demand.

“I do think people may have gotten ahead of themselves,” says Jamie Pitts. We’re sitting on the sidelines at Devcon, which was funded and organized by Pitts’s employer, the nonprofit Ethereum Foundation, which is based in Switzerland. The foundation isn’t big on titles, but Pitts is an administrator of sorts. He helps shepherd technical improvements to Ethereum’s software, a job that can be like herding real-life cats.

A soft-spoken, introspective web developer by trade, Pitts is a true believer in Ethereum, and has been since he first dug into Vitalik Buterin’s white paper in 2013. (Every cryptocurrency starts with a white paper outlining its technical principles.) He has no illusions about its current capabilities, though. “A funky computer from the ’70s,” he says with an affectionate smirk. Buterin, Ethereum’s enigmatic young creator, uses an only slightly less pejorative comparison, calling it “a smartphone from 1999 that can play Snake.”

Scores of investors and entrepreneurs had overestimated what Ethereum’s blockchain can do, and convinced others to invest billions in their projects. “They were thinking stuff like, ‘Hey I could build this medical company on the Ethereum blockchain ... and a doctor can go somewhere and their stethoscope will talk with their iPad or something over the blockchain,’ right?” Pitts says with a laugh. “CryptoKitties really put a little fear in their hearts.”

By exposing the network’s inherent weakness, CryptoKitties helped investors realize their mistake. Suddenly they became a lot more interested in Ethereum’s technical road map. “These guys are now trying to influence what happens,” says Pitts.

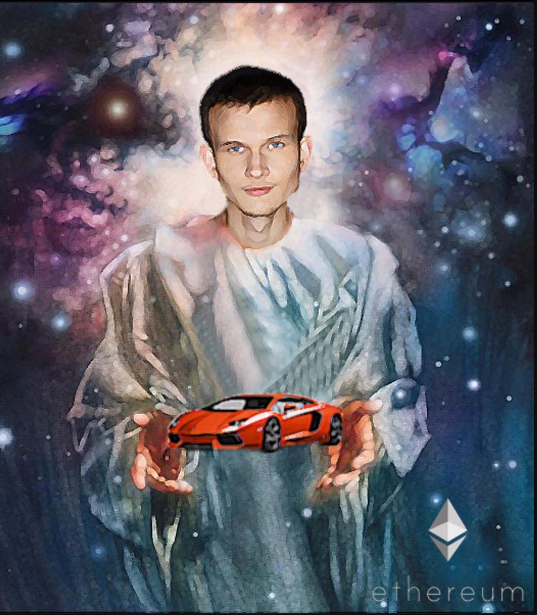

Vitalik holding a Lambo

That is why the issue of governance is such a hot topic in Prague. The mania of 2017, when cryptocurrencies shot up in value and investors piled in, made the map of Ethereum stakeholders vastly more complicated. The CryptoKitties fiasco, and a number of subsequent challenges, have made it clear that they all needed a better way to work together to solve Ethereum’s technical problems.

The afternoon before I sat down with Pitts, he and Hudson Jameson, who also works for the foundation, helped lead a sober discussion about how to create better decision-making processes.

Jameson, who has a computer science background and a friendly Texas twang, manages the most important decision-making forum that Ethereum currently has: the biweekly call between the group of self-identified core developers. The meeting can draw between 15 and 30 attendees, depending on how contentious the items on the agenda are.

Jameson often displays admirable patience during these YouTube-broadcast calls. But in Prague, there’s a hint of exasperation in his voice as he addresses a crowd of about 100 people. Complicated technical questions are testing the limits of Ethereum’s still very simple governance system, he says: “We don’t have enough people to actually help us out on these things.” That means the same people are making the decisions over and over again; the community needs better and more accessible forums for technical discussion and decision-making.

What does Ethereum’s governance look like now? Jameson asks the question rhetorically before switching to his next PowerPoint slide, which features an illustration of a cosmic-size Buterin holding a Lamborghini in his hands. (“Lambos” have become an ironic symbol of crypto-wealth.) “It’s Vitalik holding a Lambo,” he says dryly. Some in the crowd chuckle.

Jameson is mostly joking. Still, everyone knows that for all Ethereum’s ambitions to be decentralized, Buterin is still its north star. When difficult times have arisen in the past, the community has leaned heavily on him to guide them.

“Vitalik’s thinking has influenced us so much,” says Pitts. “His ethos and his outlook on life and stuff. His humility and his austerity. There are so many ways about him—even his humor—there are so many ways that he has influenced everyone here, and attracted people who had similar values.”

A geeky, gifted child whose family left Russia when he was six to move to Canada, Buterin discovered Bitcoin when he was still a World of Warcraft-playing teenager in Toronto, and he was so inspired by blockchains and cryptocurrencies that he dropped out of college to focus on them. But while Buterin loved Bitcoin, he found it limited. So he set out to design a blockchain system that could do more than just manage a store of digital values.

At 19, he published the white paper describing Ethereum. In it, he explained how he believed certain ideas from Bitcoin could be used to create a decentralized computing platform. Because it would have no single component whose failure could bring down the whole thing, and would not be subject to control by any central intermediary, such a platform could never be shut down. To Buterin, that meant freedom from online censorship, surveillance, and other forms of centralized power.

Obviously, someone with such a vision was not going to be satisfied with digital Beanie Babies. Ethereum’s mission, in Buterin’s view, is to reach the estimated 1.7 billion adults around the world who don’t have a bank account or access to a mobile money provider. Last December, when the price of Ether was soaring and the total value of all cryptocurrencies was more than $500 billion, Buterin took to Twitter to challenge blockchain developers. “How many unbanked people have we banked? How much censorship-resistant commerce for the common people have we enabled?” he asked. “Not enough.”

Ethereum 2.0

On stage at Devcon, Buterin is buoyant and optimistic about Ethereum’s future. Rail-thin, angular, and dressed in a black T-shirt and black pants, he unconsciously contorts his wiry wrists and hands as he speaks, in an almost childlike fashion, and his other movements are rather robotic. Nevertheless, the audience of nearly 3,000 developers and entrepreneurs, largely men in their 20s and 30s, is transfixed. They believe in his vision.

Buterin’s speech, which is littered with obscure jargon and acronyms, is focused on Ethereum 2.0. The label refers to “a combination of a bunch of different features that we’ve been talking about for several years, researching for several years, and actively building for several years, that are finally going come together into this one coherent whole,” he proclaims.

The problem Buterin and a few trusted collaborators have spent years laboring to crack is that the fundamental weaknesses of Ethereum, and the reasons why CryptoKitties was able to bring it crashing down, stem from the very core of how almost all existing cryptocurrencies are built.

To build an application on Ethereum, you use a specialized programming language to write so-called smart contracts. These are programs that execute automatically when certain conditions are met—for example, when the price of something falls below a certain value. Ethereum’s blockchain tracks changes to the status of all the smart contracts stored in it.

To run smart contracts, users must pay a fee in Ether, called “gas.” Gas is what keeps the whole system running. The fees ultimately go to the owners of nodes that do the mining—the costly (because it guzzles electricity) work of running the calculations that add data to the blockchain.

CryptoKitties provides a good example of how this works in practice. To create your own one-of-a-kind cat, first you need to buy one using the game’s website. A transaction on the blockchain transfers immutable ownership of the kitty to you. To “breed” your kitty with another one, just send enough gas to a smart contract on the blockchain. The game automatically mixes the “DNA” of the two parents, spits out a new kitten, and, in another transaction, stores proof that you are its sole owner on the blockchain.

Ethereum can only handle about 15 of these transactions per second, on average. Depending on how congested the network is, it can take long periods of time before a transaction becomes final. (For comparison, Visa’s payment network handles an average of 2,000 card transactions per second and has the capacity for tens of thousands.) This slowness is inherent to the design: since every node stores and processes every transaction, smart contracts are extremely difficult to disrupt or stop. The flip side is that the system is as slow as its slowest node.

Devcon teems with lively discussions about the blueprints for solving Ethereum’s technical problems. Three terms in particular—“sharding,” “Plasma,” and “Casper”—appear in nearly every talk. Slated to be part of Ethereum 2.0, together they promise to dramatically boost the system’s capacity to handle transactions without sacrificing its resilience—and substantially reduce the carbon emissions from Ethereum’s growing network of power-hungry computers.

Sharding is supposed to work by partitioning the blockchain’s data. Instead of storing and computing every smart contract, subsets of nodes would handle smaller pieces of the whole.

Plasma is a system that would let users transact with each other without always needing to go through the main blockchain. Essentially, they agree to open a private, secure communications channel and use it to do things like exchange cryptocurrency or play a game. When they are done, they can add all the updates to the main blockchain in just a single transaction.

Casper, the friendly ghost

The most ambitious project of all, however, is Casper. Spearheaded by Buterin and fellow Ethereum researcher Vlad Zamfir, it is years in the making. The goal is to reinvent the way the computers on a public blockchain network reach consensus.

To function as a decentralized network that no single entity controls, any cryptocurrency requires a consensus protocol—a process that nodes in its blockchain network use to agree, over and over again, that the information in the blockchain is valid. For Ethereum, Bitcoin, and most other cryptocurrencies, central to the consensus protocol is an algorithm called proof of work.

Proof of work works like a race. Computers designed for cryptocurrency mining devote huge amounts of processing power to repeatedly guessing at a solution to a mathematical puzzle. The first one to solve the puzzle gets to add a new “block” of valid transactions to the chain of previous ones—and receives a cryptocurrency reward. The idea behind proof of work is that would-be attackers are deterred by the massive cost of the mining hardware and electricity they would need to manipulate the ledger.

Bitcoin’s creator, Satoshi Nakamoto, did not invent proof of work but did have the inspired idea to use it as a way to make participation in a blockchain network open to the public. Anyone with the right hardware and enough electricity can mine Bitcoin, Ether, and similar cryptocurrencies—no need for permission.

Nakamoto’s consensus protocol was revolutionary. But “it’s absolutely horrible from every perspective that relates to performance,” says Emin Gün Sirer, a computer scientist and cryptocurrency expert at Cornell University. Not only is it painfully slow; it uses way too much electricity.

“The energy spent is a huge multiple of the actual energy required to build the blockchain,” says Sirer. Though Ethereum burns far less than Bitcoin, recent estimates suggest it still consumes about as much electricity as a small country, while Bitcoin uses about as much as a fairly large one. (The amounts fluctuate, but at the time of writing, Ethereum’s consumption was on a par with Costa Rica’s, and Bitcoin was roughly level with Bangladesh.)

Buterin acknowledges that this has to change. “The social impact of burning huge amounts of resources has consequences,” he told me when I caught up with him at Devcon. Billions of dollars are “wasted” via proof of work, which results in a “loss of resources that’s spread out across every single cryptocurrency user, and ultimately through all the environmental externalities, every single person in society.” It‘s also pretty bad for the brand: “Like, it could mean the difference between anyone who really cares about the environment being your friend versus trying to stop you.”

The algorithm that Buterin and his disciples have chosen as a replacement is called proof of stake. Rooted in approaches first described in the 1980s, proof of stake relies on “validators”: members of the network who, quite simply, verify and attest that transactions added to the chain are valid. Their incentive for being honest is that they must deposit, or “stake,” substantial sums of money (the current plan is 32 Ether, about $2,800 at the time of writing). When their tenure as validators ends, they can recoup the money; if they have been dishonest, they stand to lose it.

The mechanisms for choosing which validators get to add new blocks to the chain, and penalizing them for misbehavior, must be built into the algorithm. Doing that in a way that is fair and sustainable relies on solving problems in game theory, economics, and computer science. There’s also the question of how to design a system that can handle large numbers of validators without breaking down. Finally, proof-of-stake networks are vulnerable to certain malicious attacks that proof-of-work systems are not (the reverse is also true), and Ethereum’s researchers are still struggling to determine how best to defend against them.

The years-old quest to replace proof of work has proceeded in fits and starts. Promising ideas have been discarded and deadlines pushed back. That might be part of why, despite Buterin’s optimism at Devcon, his rousing speech doesn’t offer a time line for completing the upgrade.

Many of the problems confounding Ethereum’s developers have been well known for more than a decade, says Sirer, who suggests that maybe this is why Nakamoto invented a different approach for Bitcoin. “The fact that they haven’t been able to roll out a working protocol yet tells me that this is indeed a genuinely hard problem,” says Sirer. “Not just that, but the fact that nobody else has been able to do this. All the academics couldn’t do it either.”

Unicorns and rainbows

Ethereum 2.0, Buterin says, will be able to handle transaction volumes a thousand times larger than the current version, enabling it to truly become the world computer he envisioned. On stage, and later in person, he exudes a nerdy confidence that implies this is simply a matter of course.

None of the foundation employees, developers, and other attendees I speak with at Devcon express doubt in Buterin, or in the prospects for Ethereum 2.0. But some are more circumspect about the challenges.

Lane Rettig, one of the self-identified core developers, echoes Jameson’s concerns about the need for better decision-making systems: “The things we need to solve are more complex. The coordination problem is getting harder. There are more people involved, more organizations, more software.” Rettig, whose Devcon attire features black pajama pants with white-and-pink unicorns and rainbows , says that in addition to technical scalability, it is just as urgent that the community achieve “social scalability.”

A key problem Ethereum has is that the process for making changes to the software is not fully defined, says Pitts. To fix that, he and core developer Greg Colvin are spearheading a new organization called the Fellowship of Ethereum Magicians. They are modeling it after the Internet Engineering Task Force, the open, volunteer-run Internet standards organization.

All this sounds like the beginnings of a traditional institution, though, with rules and hierarchy. Doesn’t that run counter to the decentralized ideals of Ethereum?

Perhaps, but to win what Jameson calls “the blockchain wars,” it is probably going to need more structure. “There are lots of paradoxes baked in here,” admits Rettig. “You need a centralized process to invent a decentralized governance mechanism.”

Besides, many people would argue that Ethereum is already more centralized than it should be. As with Bitcoin, only a few groups of miners control most of the network’s mining power. There’s also its continued reliance on Buterin for guidance—though Buterin pushes back emphatically when I ask him if he is a single point of failure. “The dependence on me is definitely going down,” he insists.

Ultimately, what seems to unite the attendees at Devcon is not Buterin or an abstract notion of decentralization. It’s a genuine belief that Ethereum’s technology can—and should—disrupt the way humans organize themselves, and at a global scale. The question is how long its backers have to pull it off, especially if enthusiasm for cryptocurrencies continues to wane. In the end, the audacious ambition and idealism on display in Prague faces the same question Ethereum’s blockchain does: Can it scale? Or is it just CryptoKitties, unicorns, and rainbows?

Keep Reading

Most Popular

Large language models can do jaw-dropping things. But nobody knows exactly why.

And that's a problem. Figuring it out is one of the biggest scientific puzzles of our time and a crucial step towards controlling more powerful future models.

How scientists traced a mysterious covid case back to six toilets

When wastewater surveillance turns into a hunt for a single infected individual, the ethics get tricky.

The problem with plug-in hybrids? Their drivers.

Plug-in hybrids are often sold as a transition to EVs, but new data from Europe shows we’re still underestimating the emissions they produce.

Stay connected

Get the latest updates from

MIT Technology Review

Discover special offers, top stories, upcoming events, and more.