On New Year’s Day 1995, a single giant wave hit the Draupner oil

platform in the North Sea off the coast of Norway. By chance, the

platform was fitted with laser measuring equipment which recorded the

height of waves as they passed by. This one measured in at an unprecedented 25.6

metres, about the size of a seven storey office block. The Draupner

event finally confirmed the existence of rogue waves, previously

known only to science through the anecdotal evidence of the few who

had seen and survived them.

Curiously, the existence of rogue waves was predicted

mathematically more than ten years earlier by Howell Peregrine at the

University of Bristol in the UK. The theoretical prediction and the

observational confirmation should have generated an obvious question:

shouldn’t rogue waves also occur in other wave-like systems?

Advertisement

And yet it wasn’t until 2007 that the first optical rogue waves

were observed in an optical fibre. Since then things have moved

rapidly. This blog recently discussed the

first measurement of rogue microwaves and earlier this year

another group predicted the existence of rogue matter waves using

numerical simulations.

This story is only available to subscribers.

Don’t settle for half the story.

Get paywall-free access to technology news for the here and now.

But what of more abstract systems? Today Zhenya Yan at the

Institute of Systems Science in Beijing says that rogue waves can

also occur in financial systems, and in particular in equity markets.

Traditionally, econophysicists have modelled equity pricing using the

Black-Scholes economic model, in which prices change stochastically,

like the movement of particles under Brownian motion.

Researchers have long known that the Black-Scholes model cannot

account for the observed volatility of the real market but had no

alternative to turn to. However, earlier this

month, Vladimir Ivancevic at the Defence Science & Technology

Organisation in Australia proposed a nonlinear wave model as an

alternative to Black-Scholes.

The Ivancevic Option Pricing Model approximates to Black Scholes

under certain circumstances but also allows for a rich variety of

other behaviours and so has the potential to better describe real

markets. Much of this behaviour is as yet unexplored.

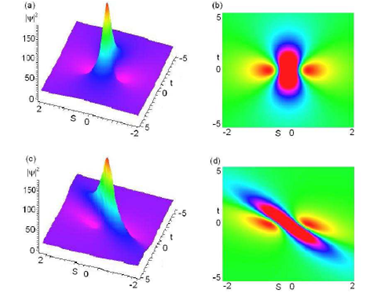

Enter Yan, who points out today that one solution of a

nonlinear wave system is a rogue wave, an event of far greater

magnitude than would be expected by any standard method of analysis.

That’s interesting. There’s no shortage of anecdotal evidence for the

existence of financial rogue waves. Look at the Asian financial

crisis of 1997 or the current global financial crisis. But

econophysicists will want more than that to confirm that financial rogue

waves really exist.

Perhaps what they need now is the financial equivalent of the Draupner oil

platform measuring ambient wave height and waiting for the big one to

hit.