China’s Latest Growth Market: Venture Capital

In 1999, when China’s per capita income was just $850 a year, a 31-year-old entrepreneur named Neil Shen and three friends nevertheless bet that China would soon develop a huge domestic tourism industry. They created a travel-booking website, Ctrip.com. China’s per capita GDP has since grown ninefold, and the domestic tourism market has ballooned to more than $400 billion. Ctrip, which had an initial public offering on Nasdaq in 2003 (and nearly doubled its price on the first day of trading), now has a market capitalization of over $10 billion—and Shen, who went on to found other travel-related companies in China, is a billionaire.

In 2005, Shen began to shift roles, from star entrepreneur to venture investor. Much like U.S. counterparts such as Netscape founder Marc Andreessen at Andreessen Horowitz or Paypal cofounder Peter Thiel at Founders Fund, Shen has made the next chapter in his career about discovering and nurturing a new generation of entrepreneurs.

He founded the independently run China affiliate of venture capital titan Sequoia Capital and now manages a portfolio that is worth, according to the Financial Times, roughly $6 billion. The range of Sequoia Capital China’s investments testifies to the energy and diversity of China’s burgeoning startup scene—from e-commerce platforms like luxury-bargain site Vipshop to science-oriented companies, including DeepGlint, which specializes in computerized 3-D image analysis; Magi, a search engine made by Peak Labs that gives answers instead of references; and drone maker DJI.

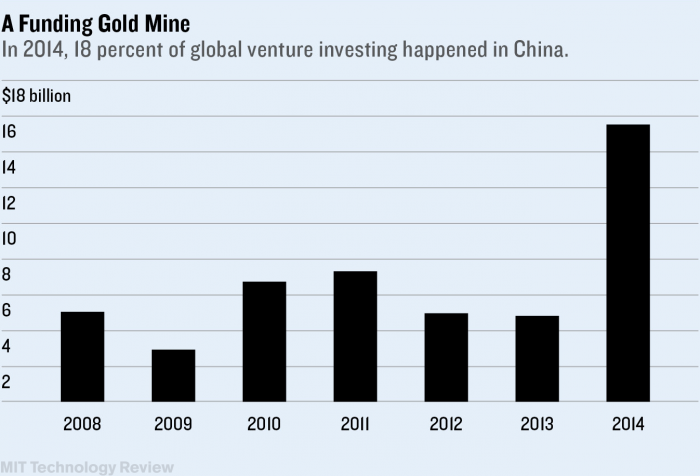

In becoming a venture capitalist, Shen was once again ahead of the curve in China. According to data from the World Economic Forum, Chinese venture capital, which had consistently accounted for roughly 9 percent of the global total from 2006 to 2013, spiked to 18 percent (about $15.6 billion) last year. PricewaterhouseCoopers recorded 1,334 venture capital deals in China in 2014, up from 738 in 2013 and 473 in 2012. Last year, China eclipsed Europe to become the second-largest destination for venture capital, after the U.S., according to the WEF.

This boom is supporting a new kind of startup investment in China—earlier- stage and riskier. The number of investors has grown, but so too has their sophistication, says Jeongmin Seong, a senior fellow at the McKinsey Global Institute in Shanghai. In 2009, early-stage investment in China accounted for 16 percent of total venture capital and angel investment, says Seong. By 2014, it had nearly doubled, to 31 percent. Investors are putting more money into early-stage deals because the competition for safer investment opportunities has become fierce. “The risk-to-reward calculation is changing,” says Rui Ma, a 500 Startups venture partner who splits her time among Beijing, Shanghai, and Silicon Valley.

Venture capital began to be available in China 10 to 15 years ago, when overseas funds started opening offices in the country to scout investment possibilities. Until then, options for would-be entrepreneurs were limited: many founders used their own savings, or pooled money from relatives living both inside and outside mainland China. Historically, China’s state-owned banks have strongly favored lending to state-owned companies, because of a widely held assumption that the government would step in to save even failing ones. That’s still true today.

This boom is supporting a new kind of startup investment in China — earlier-stage and riskier.

Zennon Kapron, founder of financial industry research firm Kapronasia in Shanghai, attributes the rise in venture capital to the class of Chinese entrepreneurs who have grown wealthy from their own companies’ public offerings. These business founders offer more than money to the startups they fund, says Kapron: “The knowledge, network, and experience that a Neil Shen can bring to the table as well is very powerful. Chinese business is still very much driven through relationships, and having that in place can be critical for any startup.”

Other Chinese tech giants that have gone public in the past decade—Baidu (2005), Alibaba (2014), and Tencent (2015)—had founders who, like Shen, went on to manage VC firms. Often called the “first generation” of China’s Internet titans, they include Alibaba’s Jack Ma, who founded Yunfeng Capital; Xiaomi’s founder Lei Jun, who launched Shunwei Capital Partners; and Pony Ma, who has overseen Tencent’s transformation into an investing powerhouse in its own right.

Their impact extends beyond their direct VC investments, inspiring the swelling ranks of both entrepreneurs and investors in China by legitimizing the startup dream. “Before, there was a huge pressure for young people to graduate college and immediately go work for a stable established company and begin to send money back home,” says William Bao Bean, a Shanghai-based partner at venture capital firm SOSV and managing director of Chinaccelerator. “Today the kids who want to launch startups can tell their parents they have role models.” In a survey of graduates from Peking University, one of China’s top colleges, only 4 percent identified as entrepreneurs or self-employed in 2005; by 2013, the proportion had grown to 12 percent.

Bob Zheng grew up in Shanghai and then went to college in Canada, where he stayed to work for consultancies for eight years. In 2008, he came back to Shanghai to launch an online education startup. At that time, it was “still a bit early for VC,” he recalls, and the initial funding came from his cofounder’s own savings. When his team sold the company in 2010, he plowed his earnings into a new business model that wouldn’t have been possible even a few years before: launching and managing co-working spaces for other entrepreneurs, called People Squared. Today, Zheng’s team runs 15 co-working spaces in Shanghai and Beijing, hosting about 250 startups, most of them tech-focused. He plans to open spaces in Hangzhou, Nanjing, and Shenzhen soon.

China’s great size is both a blessing and curse for startups: there’s opportunity to scale up quickly, but also plenty of competition. “In the U.S., if someone has an idea, maybe three other startups are working on the same idea,” says Rui Ma of 500 Startups. “In China, maybe 10 or 20 funded companies or more are competing on the same idea.”

Keep Reading

Most Popular

Large language models can do jaw-dropping things. But nobody knows exactly why.

And that's a problem. Figuring it out is one of the biggest scientific puzzles of our time and a crucial step towards controlling more powerful future models.

The problem with plug-in hybrids? Their drivers.

Plug-in hybrids are often sold as a transition to EVs, but new data from Europe shows we’re still underestimating the emissions they produce.

How scientists traced a mysterious covid case back to six toilets

When wastewater surveillance turns into a hunt for a single infected individual, the ethics get tricky.

Google DeepMind’s new generative model makes Super Mario–like games from scratch

Genie learns how to control games by watching hours and hours of video. It could help train next-gen robots too.

Stay connected

Get the latest updates from

MIT Technology Review

Discover special offers, top stories, upcoming events, and more.