Sponsored

Asia’s open banking advantage

Provided byMastercard

Open banking is one of the most significant innovation forces happening in consumer financial services around the world. It’s increasing the connectivity between banks, fintechs, and other players to improve competition within the industry and customer access to a wider marketplace of financial products and services.

Rama Sridhar is Executive Vice President, Digital and Emerging Partnerships and New Payment Flows at Mastercard.

In Europe, regulations have been significant catalysts for the rise of open banking. These include Europe’s implementation of its Second Payment Services Directive (PSD2) and the UK Competition and Markets Authority’s (CMA) Open Banking regulation. The impetus for the CMA was a 2016 investigation into competition in UK banking that found older, larger banks were not having to compete hard enough for customers’ business while smaller and newer ones were finding it difficult to access and grow in the market.

These are certainly not the same conditions that are driving financial services in Asia toward open banking. In Asia, countries are digitalizing in real-time and tech-savvy consumers are embracing e-commerce and digital payment platforms with ubiquity. To compete effectively and maintain their share of customer eyeballs and wallets, the region’s banks are largely opening up of their own accord to offer an ever-widening and innovative range of services for consumers to access and leverage their money.

This is not to say that regulation isn’t playing a role in some markets. Australia and Japan and the region’s financial powerhouses—Singapore and Hong Kong—are leveraging the lessons learned in Europe, consulting extensively with regional banks and tailoring their own approaches to fostering banking innovation.

However, because the primary driver of open banking in Asia is largely commercial, the principles of open banking—innovation, interconnectivity between banks, a dynamic ecosystem of fintechs, and consumer-centric design—are being swiftly embraced and executed on by banks and tech companies. This is particularly pronounced in China, where banks are driving open banking voluntarily with minimal regulatory mandates. As a result, they are already shaping consumers’ online experience and expectation of digital financial services.

This, combined with the rising base of financially and digitally included citizens, provides the region with the unique ability to both leapfrog to the next generation of digital financial services and learn from the first-mover regulators elsewhere. As open banking is embraced around the world, it is not a stretch to say that Asia has the potential to move to the forefront of innovation and become the global leader.

Finding their own way

Heralded as a quiet digital revolution, open banking legislation in Europe has held the attention of many monetary authorities around the world, with regulators waiting to see its net impact.

On paper, PSD2 mandates that banks create APIs (vehicles for bundling and sharing discrete data sets between organizations) for digital banking transactions, preventing consumers from being locked into a single bank’s products and services. Open banking requirements are similar, and they stipulate common standards for third parties providing information.

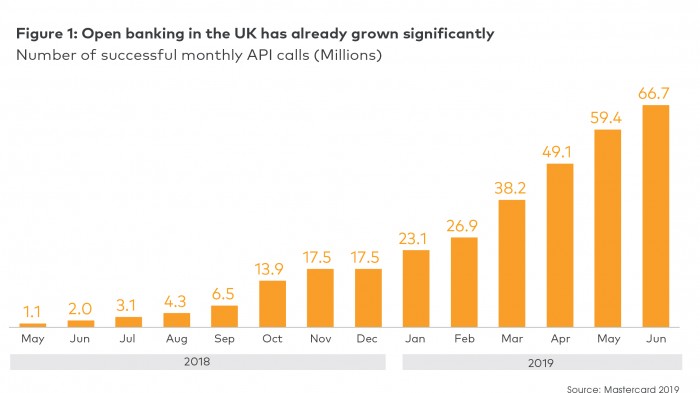

In practice, this legislation appears to be driving growth and competition in the industry—the intended effect. In the UK, API “calls” have surged over the last year, from roughly one million a month in May 2018 to more than 66.7 million in June this year. A recent report commissioned by the Open Banking Implementation Entity (OBIE) estimates that UK consumers and businesses will see £18 billion ($22 billion) in additional value annually because of the increased levels of service and competition brought about by open banking.

As a result, regulators in Asia are now seeking to create legislation that creates the conditions where an open banking ecosystem can flourish in their own markets. Australia’s federal government made it a requirement for major banks to provide product information APIs by July of this year, and it will require them to make all consumer and transaction data open and available by July 2020. Japan’s regulators have strongly encouraged banks to publish APIs, and an amended Banking Act is expected to encourage 80 major retail banks to open their APIs by 2020.

Elsewhere, “sandbox” style collaborations between banks, fintechs, and regulators have propelled debate about the direction that open banking activities should take and accelerated the development of APIs in the region. In July 2018, the Hong Kong Monetary Authority (HKMA) published an open banking API framework developed in collaboration with industry stakeholders, which is already gaining traction. Since the beginning of 2019, some 20 retail banks in Hong Kong have launched more than 500 open APIs for product information, and will participate in a second phase, involving APIs for loans, credit cards, and other new applications, in October this year.

Similarly, the Monetary Authority of Singapore (MAS) published an API Playbook last year; to date Singapore’s API Register has logged 121 transactional and 192 informational APIs. In 2017, Singapore’s largest bank, DBS, launched what it claims is the world’s largest API development platform for fund transfer and other services of its own digital bank and those of partners such as PropertyGuru, AIG, and FoodPanda.

And in May this year, Thailand’s Siam Commercial Bank (SCB) created an API development portal, through which it will share technology for such applications as QR payment code development, customer profile development, and authentication with partners.

These initial steps have already been quite transformative to the adopting country’s digital transaction landscapes. For example, within 10 months of its launch following the API publishing requirements, PayPay, a Japanese smartphone payment settlement service, registered 10 million customers and more than 100 million transactions. In Hong Kong, 200 APIs from 13 banks have been launched on the Jetco APIX platform, and Singapore has 313 APIs currently available in the MAS API register. In China, all major banks are offering APIs across various services.

Keeping pace with the market

While Asian monetary authorities are currently taking a lighter regulatory approach than their European counterparts, this does not mean the pace of innovation is any more relaxed. Indeed, banks in the region are being rapidly propelled into open banking territory by the pace of fintech advancement in the markets themselves. The incredible speed at which Asia is digitalizing—particularly in the financial sector—is largely being driven by the proliferation of mobile transaction platforms, rising consumer acceptance for digital banking channels, and increasing efforts by Asian governments to promote cashless societies.

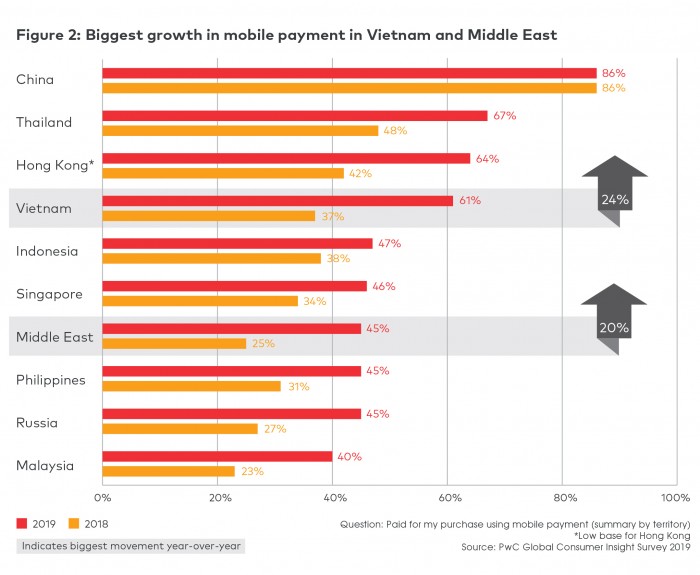

A recent survey by PwC estimates that eight of the world’s 10 fastest-growing mobile payment markets are in Asia, led by Vietnam, where more than 60% of consumers regularly make transactions over smartphones. Google estimates that some $1 billion in cashless (largely mobile-payment-based) transactions were conducted in 2017 on local digital commerce platforms, such as ride-sharing giants Grab or Go-Jek, or e-marketplaces such as Tokopedia. In China, over half of point-to-point transactions today are conducted through either AliPay or WePay, according to WalkTheChat, a WeChat marketing consultancy, with a total estimated value of more than $122 billion.

As a result, in many Asian markets, it is the “digitally native” internet businesses, rather than traditional banks, that are opening up the financial landscape. Many of these innovators, in India and China in particular, have generated such scale and market influence that they have also acquired government support and sponsorship of their new banking service models they advocate.

In order for Asia’s traditional banking industry players to compete effectively and maintain their status in consumers’ financial lives, they have one choice—to fully digitalize products, services, and customer experiences. If traditional banks are keen to exploit these new opportunities, they must, in effect, share their hard-won customer relationships with the wider ecosystem of digital services, giving consumers the convenience and choice they are coming to expect. This ultimately requires banks to adopt open banking principals, and keep pace with consumer demands for flexible and seamless digital services.

While many financial services leaders in Asia would admit that the long-term implications of open banking on customer relationships and the market landscape are still uncertain, most are approaching the new ecosystem with a high degree of proactivity and optimism. Traditional banks are being innovative in developing APIs and new services, and taking advantage of new regulatory opportunities.

For example, Standard Chartered Bank, which has a 166-year history, has been awarded one of the eight “virtual banking” licenses issued by HKMA since March 2019. Another recipient is Ping An Insurance, China’s technology-forward insurance market leader. Ping An’s OneConnect Bank is scheduled for a soft launch at the end of 2019, but has already been working with other financial service providers in China and across Asia to provide technology services based on its API-driven service model.

In contrast, banks that fail to embrace open banking simply will not be able retain customers and relevance in this landscape. For example, the entry of digital banks—which are becoming a global runaway phenomenon—has already begun to disrupt retail banking services in Asia and beyond. They point toward the future of banking: virtual institutions that do not charge minimum balance service fees and offer competitive lending fee structures that will ultimately outcompete traditional banking model.

Firm foundations

Without strict regulatory mandates, Asia’s organic, collaborative, and market-led path toward open banking could make its financial services industry even more innovative and dynamic than Europe’s. Indeed, if the goal is to create seamless end-to-end experiences where, in the absence of silos, and customers are truly free to access any number of service providers and benefit from a financial services landscape where large and small players have equal access and opportunity, it is conceivable that Asia will reach this point before any other region in the world.

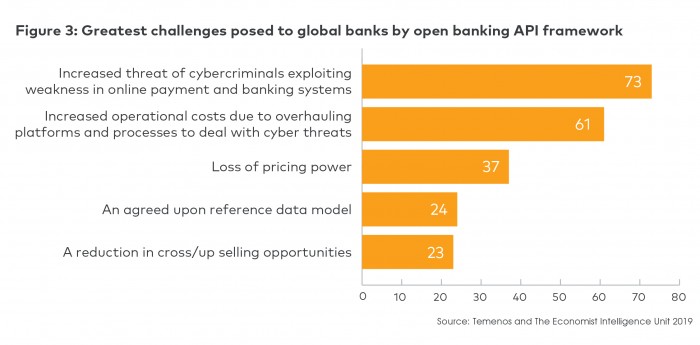

Yet there are challenges to this light hand. Important issues such as consumer data protection and security have the potential to be neglected as Asian players race pell-mell to establish presence. Indeed, cybersecurity is emerging as one of the most significant challenges to banks as they look to adopt open banking frameworks.

Consumers must also be brought along for the journey, including those who haven’t yet entered the financial system.

As a result, for Asian ecosystem players to leapfrog to the head of the race to open up the financial services landscape, banks and ecosystem players in the region need to ensure three key areas are adequately addressed:

Security must underpin the whole system. Rapid innovation in an open ecosystem creates many opportunities for consumer data to be hacked or misused, and the proliferation of connections has the potential to create a mess of permissioning.

As a result, authentication systems for enhancing security around customer data integrity are essential for giving open banking ecosystem participants the confidence that customer data provided by partners or customers themselves is in fact genuine.

It is for this reason that Europe’s PSD2 insists that banks deploy common Strong Customer Authentication (SCA) standards. However in Asia, authentication tools are as of now are being providing through collaborative industry frameworks or sandbox development portals such as SCB launched in Thailand.

As a result, stronger cybersecurity measures are needed in the region. Further, setting the bar for regional cybersecurity collaborations could underpin Asia’s ability to leapfrog. If policymakers and monetary authorities across the region can collaborate together to mitigate risk and build trust in innovative financial services, the ecosystem will proliferate for all stakeholders—banks, fintechs, and consumers.

Consumers need to be brought on the journey. As banks enter new partnerships and develop new APIs at a breakneck pace, they need to make sure that they are creating the services that provide the most value for consumers and don’t overwhelm them with needless choices. Customer education must also include building trust in the security behind data transfer mechanisms so that consumers are confident to use the services available to them.

Ensuring consumers are brought along for this journey will help ease the friction the UK is currently experiencing in trying to accelerate the pace of change. According to a recent survey of 2,000 people by Splendid Unlimited, only one in four people have heard of open banking and only one in five knew what it meant or entailed. Beyond this, respondents were reported to be cynical that open banking is more for the financial services industry than for them, which doesn’t help progress.

Companies need to balance innovation with inclusion. With competitors popping up almost daily to challenge banks for their digital consumers, it is worth remembering that large swaths of Asia are still largely unbanked and in need of simple and secure access to financial services. There are tremendous gains to be made by banks in continuing to promote financial inclusion for the millions at the lower end of Asia’s socioeconomic spectrum. In developing digital banking strategies, banks should continue to keep financial inclusion as a high priority area for innovation.

In short, by simultaneously harnessing keen, focused attention from its regulators and the appetite for digital convenience and choice of its consumers, Asia's financial service industry stands to create an innovative and competitive open banking marketplace. In fact, Asia's unique blend of digital market savvy and “light-touch” policymaking may see it become a global open banking leader.

However, for this to happen in a robust and sustainable way, Asia's banking ecosystem participants must also temper their organic market-minded drive with systematic and collaborative adoption of key fundamentals including appropriate security practices and market education efforts.

Deep Dive

Computing

Inside the hunt for new physics at the world’s largest particle collider

The Large Hadron Collider hasn’t seen any new particles since the discovery of the Higgs boson in 2012. Here’s what researchers are trying to do about it.

How ASML took over the chipmaking chessboard

MIT Technology Review sat down with outgoing CTO Martin van den Brink to talk about the company’s rise to dominance and the life and death of Moore’s Law.

How Wi-Fi sensing became usable tech

After a decade of obscurity, the technology is being used to track people’s movements.

Algorithms are everywhere

Three new books warn against turning into the person the algorithm thinks you are.

Stay connected

Get the latest updates from

MIT Technology Review

Discover special offers, top stories, upcoming events, and more.