Technology Repaints the Payment Landscape

In developed economies, money has been digitizing for decades. Few Westerners touch a paycheck anymore. Through direct deposit, digital money is transferred electronically from our employer to our bank account every pay period. A similar process moves contributions into our 401(k) accounts or zaps money over to pay the rent, the utility bill, a student loan, or any other expense.

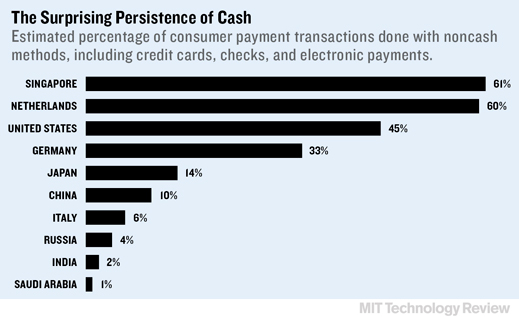

Yet it remains a cash-based world, with 85 percent of consumer transactions worldwide done with bills and coins. While some countries, like Singapore and the Netherlands, now use cash in a minority of payments, consumers in such diverse economies as India, Mexico, Italy, and Taiwan still execute more than 90 percent of transactions with cash, according to research by MasterCard Advisors. Even in the United States, they find, cash accounts for 55 percent of payments. New technologies, including digital wallets, cryptocurrencies, and mobile peer-to-peer payments, aim to tip that balance. They’re accelerating the move away from cash in countries where alternatives to banks and credit cards are well established, and they’re doing the same in developing economies.

Which technologies and companies are likely to lead this transformation is the big question for this Business Report.

One way to look at these new technologies is through their relationship with the long-established payment services. Some technologies, including the mobile wallets Apple Pay and LoopPay, run on top of the existing payment networks owned and operated by banks and credit card companies. The new technologies are designed to make those established systems faster, more convenient, or more secure, and to convert transactions now being done in cash. A different group of technologies would replace the established systems with new ones, fundamentally challenging the vast industry that executes, guarantees, and tracks payments. Among them: Venmo, a person-to-person payment app and social network that processes $3 billion of payments a year, and Dwolla, an upstart in Iowa looking to cut the payment-processing revenue enjoyed by Visa and other networks.

As technology drives a shift in how we buy things, the revenue that the payments industry extracts could grow to more than $2 trillion a year by 2023, double the 2013 figure, the Boston Consulting Group predicts. Much of that increase will come from a reduction in cash payments in developing countries. But across the globe, BCG predicts a time of “disruption and opportunity” driven by digital technologies that will require the existing credit card system to prove that it’s better than its new competition.

“The smartphone is the catalyst for a lot of change in this industry,” says Dana Stalder, a venture capitalist with Matrix Partners and a former eBay and PayPal executive now on the board of Poynt, which recently introduced a smart credit card terminal. Venture capitalists invested over $2 billion in payment technology firms between January 2013 and June 2014, according to the data tracking firm CB Insights.

However, established players, especially the banks and credit card companies that handle most noncash payments today, have, if anything, seen their positions strengthened by recent developments. A good example is the high-profile launch of Apple Pay. Unlike earlier technologies like Google Wallet and PayPal, Apple Pay makes no attempt to supplant the Visas and Bank of Americas of the world. Look at your digital wallet in Apple Pay and you see a version of exactly the same card as in the wallet in your pocket. The digital wallet LoopPay, which can be used in many more terminals than Apple Pay because it uses a simple, widely compatible copper loop technology to simulate the coding in your credit card’s magnetic strip, similarly relies on the existing credit card system.

“Think about the infrastructure and how long it took to create that,” says LoopPay CEO Will Wang Graylin. “It’s very difficult to change merchant behavior.”

Innovation in payments might be especially likely to take hold in the developing world, where cash is still king. Leapfrogging ATMs and checks the same way they have skipped over landlines and cable, whole chunks of population are moving straight from cash to mobile money. M-Pesa, which has become a force in Kenya and Tanzania, has turned money into a cellular currency that can be converted into airtime or used to pay for things. Today, some 60 percent of Kenyan adults have used a mobile phone to receive or send payments.

What could derail the boom in payment technologies?

Security concerns. The consulting firm Accenture recently surveyed 4,000 consumers in North America and found that while more people expect to use mobile payments, 57 percent of respondents were concerned about the security of such transactions. That’s up from 45 percent two years ago.

New approaches could help. Apple Pay, Google Wallet, and others utilize a system that creates a one-time digital token for each transaction and sends that, rather than a customer’s credit card information, through the system.

Innovations like this show that mobile payments—even if they don’t lead to a radical shake-up—are improving a global payment ecosystem that’s long been due for an upgrade.

Keep Reading

Most Popular

Large language models can do jaw-dropping things. But nobody knows exactly why.

And that's a problem. Figuring it out is one of the biggest scientific puzzles of our time and a crucial step towards controlling more powerful future models.

How scientists traced a mysterious covid case back to six toilets

When wastewater surveillance turns into a hunt for a single infected individual, the ethics get tricky.

The problem with plug-in hybrids? Their drivers.

Plug-in hybrids are often sold as a transition to EVs, but new data from Europe shows we’re still underestimating the emissions they produce.

Google DeepMind’s new generative model makes Super Mario–like games from scratch

Genie learns how to control games by watching hours and hours of video. It could help train next-gen robots too.

Stay connected

Get the latest updates from

MIT Technology Review

Discover special offers, top stories, upcoming events, and more.